Artificial intelligence has become the latest excuse for reviving one of the oldest bad ideas in economic policy: a universal basic income. Recent pieces in Newsweek, the LSE Business Review, and Fortune have all helped push the idea that AI may soon wipe out so many jobs that Washington will need to send everyone a check.

That makes for a catchy headline. It also makes for terrible economics.

The right question is not whether AI will disrupt work. Of course it will. The right question is this: after more than 100 local guaranteed-income experiments, what have we actually learned?

The answer is much less flattering to UBI than its promoters would like.

What 122 UBI-Style Pilots Show

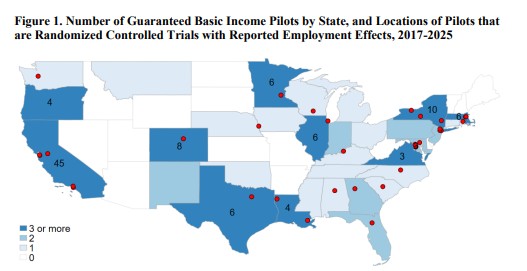

A new AEI working paper by Kevin Corinth and Hannah Mayhew gives the best recent overview of the evidence. Per their study, there were 122 guaranteed basic income pilots across 33 states and the District of Columbia between 2017 and 2025. Those pilots allocated about $481.4 million in transfers to 40,921 recipients, with 61,664 total participants including control groups. The average recipient got about $11,765, the average pilot lasted 18.4 months, and the average monthly payment was $616.

That sounds like a mountain of evidence. It is not.

Of those 122 pilots, only 52 had published outcomes. Only 35 used randomized designs. Only 30 reported employment outcomes. So the case for UBI is not being built on some giant pile of clear, clean evidence. It is being built on a much smaller stack of studies, many of them weak, limited, or badly timed.

And here is the kicker. Among the 30 randomized pilots with published employment results, the average effect was a 0.8 percentage-point increase in employment. UBI fans will rush to wave that around. They should slow down.

AEI shows that the bigger and more credible studies tell a very different story. Among the four pilots with treatment groups of at least 500 participants, which together account for 55 percent of all treatment-group participants, the mean effect on employment was minus 3.2 percentage points. AEI also estimates a mean income elasticity of -0.18, which is consistent with standard labor-supply economics.

In plain English, when people receive more unearned income, work tends to fall at the margin. Shocking, I know. Economics still works.

Credit: American Enterprise Institute

Why the Evidence Is Weaker Than the Hype

The AEI paper is useful not just for what it finds, but for how bluntly it describes the weaknesses in the evidence.

The average treatment group among those 30 studies was just 359 people, and the median was only 151. That is not exactly ironclad evidence for redesigning the American welfare state. Among the 26 pilots for which attrition could be measured, the average attrition rate was 37 percent. That is a giant warning sign. If enough people drop out, the reported results can become badly distorted.

The studies also varied widely in payment size, duration, sample composition, and even how outcomes were measured. The mean annualized payment was $7,177, equal to an average income boost of about 39.5 percent relative to baseline household income in the studies. Some pilots relied heavily on self-reported survey data. Some were conducted during or right after the COVID period — when labor markets, safety-net programs, and personal decisions were anything but normal.

AEI’s conclusion is appropriately cautious: these findings may not generalize to a permanent, universal, nationwide UBI under current or future conditions. That alone should cool off a lot of the AI-fueled policy hysteria.

AI Will Displace Jobs. It Will Also Create Them

None of this means AI will be painless. Some jobs will shrink. Some tasks will disappear. Some workers will need to retrain, relocate, or rethink their careers. That is what happens when productivity rises and technology changes how goods and services are produced. It happened with mechanization, with computers, and with the internet. It will happen with AI.

But displacement is not the same thing as permanent mass unemployment. That leap is where the UBI argument falls apart. Economies are not fixed piles of jobs. They are dynamic systems of discovery, adaptation, and exchange. When costs fall and productivity rises, resources move. Businesses reorganize. Consumer demand changes. New occupations emerge. Old ones evolve. Some disappear. That churn is real, but so is the adaptation.

The answer to technological change is not to pay people for economic resignation. The answer is to make adaptation easier.

UBI Fails the Economics Test

There is a reason Ryan Bourne at Cato has argued that UBI is not the answer if AI comes for your job. It confuses a transition problem with a permanent income problem. Worse, it assumes that writing checks can substitute for the incentives, signals, and institutional conditions that actually create opportunity.

UBI also crashes into the budget constraint. As Max Gulker at The Daily Economy has noted, UBI is often sold through small pilots and vague moral language, but the national arithmetic is ugly. And as Robert Wright in another AIER piece points out, “universal” quickly means sending money to many people who are not poor while piling enormous costs onto taxpayers. (Bear in mind, the national debt is already rapidly approaching $40 trillion.)

That is before getting to the public-choice problem. In theory, UBI supporters sometimes imagine replacing the welfare state with one simple cash transfer. In reality, government programs rarely disappear. Bureaucracies defend themselves. Interest groups protect carveouts. Politicians promise more, not less. So a UBI would likely be stacked on top of much of the current welfare state, not substituted for it. That is not reform. That is fiscal delusion with better branding.

A Better Answer: Remove Barriers to Work

If AI means more labor-market churn, then policy should focus on mobility, flexibility, and self-sufficiency. That means less occupational licensing, lower taxes, lighter regulation, fewer benefit cliffs, less wasteful spending, and more room for entrepreneurship and job creation. The government should stop making it harder for people to pivot.

It also means reforming welfare the right way. My proposal for empowerment accounts is not a UBI. It would be targeted to people already eligible for welfare, not universal. It would include a work requirement for work-capable adults, not detach income from effort. And it would consolidate fragmented programs into a more flexible account that families control directly, reducing bureaucracy and lowering spending over time as more recipients move toward self-sufficiency.

That puts it much closer to the classical liberal insight behind replacing bureaucratic control with direct support, while avoiding the fatal error of turning the entire country into a permanent transfer state. As Art Carden reminds us at The Daily Economy, there is a long intellectual history behind cash-based assistance. But today’s UBI politics are not really about shrinking the state. They are mostly about expanding it because elites fear AI.

Don’t Make Bad Policy Out of Fear

The UBI revival tells us less about AI than it does about politics. New technology arrives, uncertainty rises, and too many policymakers reach for the federal checkbook as if it were a magic wand. It is not.

After 122 local experiments, the case for UBI is still weak. The best evidence does not show a jobs renaissance. The larger studies show employment declines. The broader evidence base is riddled with small sample sizes, high attrition, and limited generalizability. That is a flimsy foundation for a permanent national entitlement.

AI will change work. It will not repeal economics. The best response is not fear-driven universal dependency. It is a freer economy with stronger incentives to work, save, invest, adapt, and prosper.