Wars test nations. They test military readiness, alliance cohesion, and political resolve. But they also test something less visible and just as important: fiscal strength.

Just days before the United States entered war with Iran, President Trump was arguing for a $500 billion defense spending increase. The Washington Post reported that administration officials were struggling to justify such a massive military budget blowout in this year’s executive budget proposal, while warning about what it would mean for an already crisis-level federal deficit.

Although the absurdity of President Trump’s arbitrary defense budget request hasn’t changed, the terms of the debate have. Whether justified or not, war places immediate pressure on defense budgets. The real question is whether the United States has put itself in a position to afford it.

Washington politicians have spent irresponsibly in times of peace and war, during economic expansion and contraction, through pandemics — you name it.

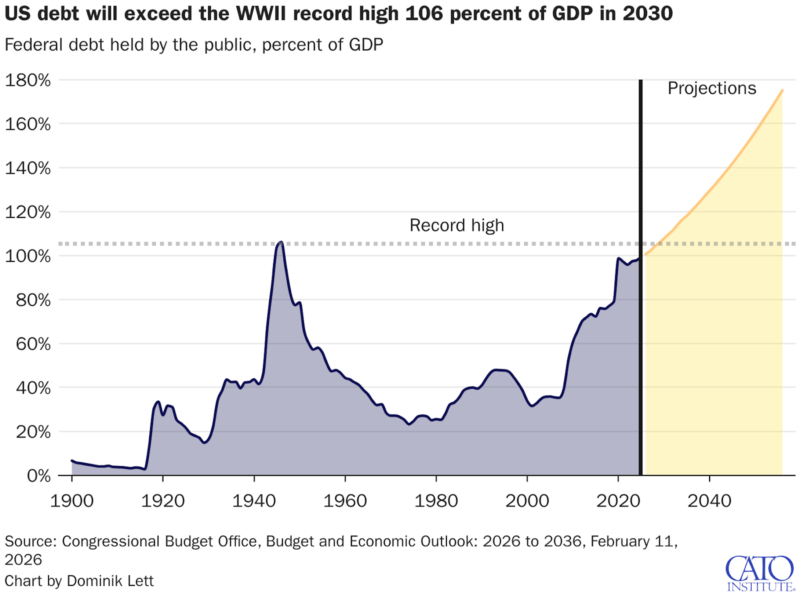

Debt held by the public is already near historic highs as a share of the economy and is surpassing its World War II record high in fewer than four years. According to the Congressional Budget Office (CBO), the federal government is projected to continue running structural deficits indefinitely, with debt rising to fiscally dangerous levels over the next few decades.

This is not the result of war mobilization. It is not the result of an economic collapse. It is the consequence of congressional cowardice paired with fiscal indiscipline.

This deterioration has not been driven primarily by defense spending or even by temporary war outlays. Over the past 35 years, Congress has enacted roughly $15 trillion in emergency spending and associated interest costs, according to research by Cato Institute budget analyst Dominik Lett — responding to wars, recessions, natural disasters, and the pandemic.

But what distinguishes the current moment is not the existence of an emergency spending spike. It is the failure to reverse course afterward. Since the COVID-19 pandemic, crisis-level deficits have become routine, not emergency measures.

Throughout American history, large temporary increases in federal spending — during World War II, the Cold War, the Great Recession, and the COVID-19 pandemic — were possible because bond markets had confidence in the long-term stability of US public finances. Investors were willing to absorb additional Treasury issuance because the underlying fiscal foundation was perceived as sound.

But unlike after World War II, the COVID-19 emergency spending spike was not followed by congressional resolve to reduce deficits. Instead, deficits have stayed elevated as entitlement spending continues climbing on autopilot, with spending on the elderly projected to consume half of the entire federal budget in just a few years. To add insult to injury, Congress further increased Social Security and Medicare benefits to curry favor with voters and cut taxes without cutting spending commensurately.

The United States government is borrowing at crisis levels even in normal times and testing bondholders’ confidence in US fiscal management.

National security leaders across eight Republican and Democratic administrations warned a decade ago: “Long-term debt is the single greatest threat to our national security.”

Excessive debt slows economic growth, reduces income levels, raises interest rates, and constrains funding for core government functions, like national defense.

Ironically, fiscally irresponsible emergency spending in the name of national security can make the country less safe. A fiscal crisis would erode America’s military and economic strength simultaneously. High debt can also magnify the severity of future crises by limiting the government’s capacity to respond.

This is the paradox now confronting Washington. The case for spending more on defense will only grow louder now that the country is at war. But financing a larger military by borrowing yet more, when interest costs on the existing debt already exceed what the nation spends on defense, becomes fiscally untenable.

When politicians spend every year as if we are confronted with an emergency and treat every special interest group’s request as a priority, they diminish the nation’s capacity to respond when a real emergency arrives.

Rising interest costs are consuming a growing share of federal revenues, with the CBO projecting that major entitlement programs, Medicare, Medicaid, Social Security, and interest on the debt will consume all tax revenues by the end of this decade. And this was before the United States decided to get involved in an active battle in the Middle East.

With US debt approaching the size of the economy, even modest increases in interest rates significantly raise borrowing costs. Every dollar devoted to servicing past debt is a dollar unavailable for current government functions, including defense. When bond markets begin to question America’s fiscal trajectory, borrowing costs could rise even higher, and do so quickly.

America’s defense should not depend on the assumption that investors will always finance unlimited deficits at favorable rates. Fiscal security is a prerequisite for military security.

Running sustainable budgets in normal years preserves borrowing capacity for extraordinary circumstances. It ensures that when genuine emergencies arise, the government can respond decisively without risking financial instability.

If Congress decides that military needs require higher spending, legislators should identify offsets elsewhere in the budget. Emergency funding should not become an excuse for permanent fiscal expansion. Congress is already discussing a possible emergency supplemental to finance the war against Iran, while some have suggested doubling down on reconciliation to boost military expenditures without requiring Democrats to support such a package.

If Congress continues current fiscal practices — running multi-trillion-dollar deficits while increasing spending and cutting taxes — the country may soon discover that there is a limit to how much debt US bondholders will tolerate before inflation expectations adjust. Higher interest rates soon follow, potentially triggering a vicious debt doom loop, where higher debt drives up interest rates, which then drives up debt, and so forth. An accommodating Fed would only add to those inflation expectations, should monetary policy surrender to the Treasury’s immediate financing needs. This is not a theoretical concern. It is a strategic vulnerability.

In times of peace, balance sheets matter. In times of war, they matter even more.