Campaigning for a second term, President Donald Trump committed the United States to sweeping tariffs that have no precedent since the Second World War. Shortly after his inauguration, Trump issued multiple Executive Orders (EOs) and press releases both to enact and sometimes reverse tariffs. Anticipation, enactment and then pauses in the president’s tariff agenda all affected US and global equity markets. This essay reports on the market impact of Trump’s multiple tariff decisions.

Table 1 summarizes values, as of April 30, 2025, for several US and foreign equity markets. It also reports our calculations of daily positive and negative market value changes resulting from Trump’s tariff decisions between election day (November 5, 2024) and April 30, 2025. The daily events are summarized in table 2 below. Cumulative changes at the foot of table 1 represent the summation of negative and positive daily changes following tariff event days, not total market changes between November 5, 2024, and April 30, 2025.

The cumulative negative impact of decisions imposing tariffs subtracted $377 billion from the market value of the Russell 2000, $2 trillion from the Magnificent Seven, $4.7 trillion from the S&P 500 (which includes the Magnificent Seven), and $2.2 trillion from the market value of equities in six seriously affected foreign countries.

Market losses were sharply reversed when Trump paused pending tariffs on April 9, 2025. Excluding the rebound following the April 9 pause, the negative daily changes far exceeded the positive daily changes. oreover, US shares were by far the biggest loser from Trump’s tariffs, especially the Magnificent Seven.

Table 1. Daily market capitalization changes between November 4, 2024, and April 30, 2025. $ billion.

Source: Bloomberg and authors’ calculations.

Notes: For each country, the following indexes represent the respective equity markets: Mexico (S&P/BMV IPC, ticker: MEXBOL), Canada (S&P/TSX Composite, ticker: SPTSX), China (CSI 300, ticker: CSI300), Europe (STOXX Europe 600, ticker: STOXX600), Japan (Tokyo Stock Price Index, ticker: TOPIX), Korea (Korea Composite Stock Price Index, ticker: KOSPI). Cumulative one-day impact is the sum of daily changes following tariff events. Since the February 1 announcement was on a weekend, February 3 was used as an approximation. For China, February 5, 2025, was the first trading day of the month due to national holidays and was thus used to approximate the reaction to the tariff announcement on February 1 (*).

US Equity Market Reactions

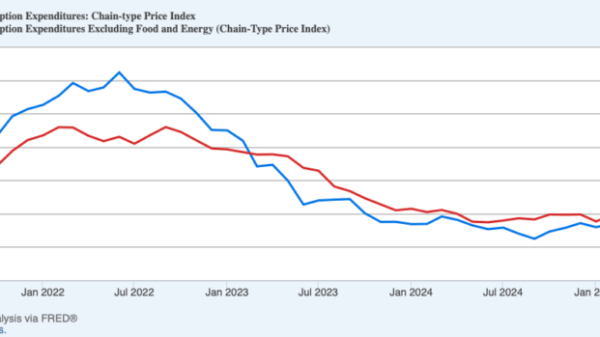

Figure 1 depicts US equity markets for two quite different share categories – the Russell 2000 and the Magnificent Seven – beginning with the general election on November 5, 2024, and ending on April 30, 2025. The Russell 2000 index includes approximately 2,000 small-cap US equities, firms with limited exposure to foreign trade or investment. By contrast, the Magnificent Seven are highly successful tech firms deeply engaged in world markets, both through trade and investment: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla.

As figure 1 shows, the Russell 2000 index rallied after Trump’s election, but then lost most of those gains by inauguration day. The Magnificent Seven, however, enjoyed a stronger and more durable rally, gaining about 20 percent between election and inauguration. Evidently, investors believed that Trump’s policies would be highly favorable, at least for large tech firms.

On inauguration day and in the following weeks, Trump issued multiple Executive Orders (EOs) decreeing far higher and more comprehensive tariffs than markets had anticipated. Gloomy prospects of domestic inflation, foreign retaliation, and business chaos shocked the financial markets. Both the Russell 2000 and the Magnificent Seven indexes fell sharply until Trump announced a dramatic tariff pause on April 9, 2025.

Figure 1. Russell 2000 and Magnificent Seven market indexes.

Source: Bloomberg and authors’ calculations.

Notes: Each index is normalized to 100 based on its own value on November 4, 2024. This allows for a direct comparison of relative performance over time.

Digging deeper, we explore equity market valuation changes immediately following each Trump tariff announcement. For this exercise, we examine the change in market prices between the close on the previous day and the close on the announcement day. But for “reciprocal” tariffs that were announced after the market closed on April 2, 2025, we examine the change between the close on April 2, 2025, and the close on April 3, 2025.

Invoking the efficient market hypothesis, we assume that the expected effects of an announced tariff change on corporate earnings, interest rates and other factors are quickly reflected in equity valuations. Initial expectations may prove too pessimistic or too optimistic. The efficient market hypothesis, however, asserts that immediate expectations as to the price effects of a shock provide the best available forecast on that day. Further, by attributing all valuation changes on the announcement dates to tariff changes, we assume that other contemporaneous shocks were generally minor.

Table 2 lists the dates and summarizes the content of Trump’s tariff announcements, starting with his election on November 5, 2024. Election day is included because market participants then knew that major tariff changes were a near certainty. Trump’s inauguration day, January 20, 2025, was also included because that marked the beginning of specific tariff decisions. Table 2 further shows the percentage change on each valuation day of an ETF for the Russell 2000 (IWM) and the Bloomberg index (BM7P) for the Magnificent Seven. The daily percentage changes in table 2 provide the basis for calculating the daily dollar changes in table 1.

On most valuation days, the Russell 2000 and Magnificent Seven share the same direction of change and roughly similar magnitudes. For example, following the “reciprocal” tariff announcement on April 2, 2025, the Russell 2000 dropped 6.3 percent, while the Magnificent dropped 6.7 percent

At the foot of table 2, the first row summarizes cumulative negative market reactions recorded on valuation days, expressed in percentage terms. Perhaps surprising, the Russell 2000 index dropped almost as much as the Magnificent Seven.

The second row at the foot of table 2 summarizes cumulative positive market reactions recorded on valuation days, expressed in percentage terms. In total, positive market reactions exceeded negative market reactions, thanks to the huge relief rally when Trump paused tariffs on April 9, 2025.

The third row at the foot of table 2 summarizes cumulative positive reactions in percentage terms, apart from the April 9 relief surge. Evidently, without the tariff pause, the Russell 2000 index and the Magnificent Seven would both have been deeply in the red at the end of April 2025.

Table 2. One-day price returns of Russell 2000 and Magnificent Seven on Trump announcement days. Daily percent changes.

Evaluation Day

Event

Russell 2000, 1-day returns (%)

Magnificent Seven, 1-day returns (%)

11/5/2024

Election Day

1.9

1.8

1/21/2025

Inauguration Day (Jan 20, 2025)

1.8

0.3

2/3/2025

On February 1, Trump issued EO announcing tariffs on Canada, Mexico, and China.

-1.3

-1.7

2/10/2025

Trump announced 25 percent import tariffs on steel and separate proclamation imposing 25 percent tariffs on aluminum as of March 12.

0.4

0.4

3/4/2025

EOs to raise the new tariffs on all imports from China from 10 percent to 20 percent, impose 10 percent tariffs on imports of Canadian oil and energy products and 25 percent tariffs on the remainder of imports from Canada.

-1.1

-0.6

3/25/2025

The White House issued secondary tariffs on third countries importing Venezuelan oil.

-0.7

1.2

3/26/2025

The White House imposed 25 percent tariffs on automobiles and certain automobile parts.

-1.0

-3.0

4/3/2025

On April 2, the White House invoked IEEPA to impose baseline 10 percent tariff starting April 5 and then “reciprocal” tariffs starting April 9.

-6.6

-6.7

4/8/2025

The White House amended to impose additional 50 percent tariff on imports from China, increasing to 84 percent.

-2.7

-2.4

4/9/2025

The US imposed an additional country-specific tariff on China; then paused other “reciprocal” tariffs for 90 days, except for China. China will now face 125 percent of tariffs.

8.7

14.4

4/11/2025

The White House issued a list of products, including smartphones and semiconductors, to be excluded from the April 2 executive order

1.6

1.9

4/29/2025

The White House issued a proclamation and an executive order to address concerns over stacking tariffs and avoiding the cumulative tariffs. The proclamation also amended previous tariffs under Section 232 regarding automobiles and automobile parts.

0.6

0.6

Cumulative one-day loss (%)

(13.4)

(14.4)

Cumulative one-day gains (%)

14.9

20.6

Cumulative one-day gains (%), without April 9

6.2

6.2

Source: Bloomberg and authors’ calculations. Bown, Chad P, “Trump’s Trade War Timeline 2.0: An Up-to-Date Guide.”

Notes: One-day price returns are calculated by the percentage change between the closing price on the announcement day and the closing price on the previous trading day.

The equity market surge, following the tariff pause on April 9, 2025, was a game-changer, not only for the markets but also for Trump’s political fortunes. According to press reports, Commerce Secretary Howard Lutnick and Treasury Secretary Scott Bessent sold Trump on the pause, overshadowing tariff hawk Peter Navarro.

If that account is accurate, Lutnick and Bessent gave Trump good advice. Without the pause, equity market losses for the six months between November 2024 to April 2025 would have overwhelmed equity market gains.

Foreign Equity Market Reactions

Figure 2 compares the S&P 500 index with indexes of exchange-traded funds (ETFs) for six affected countries. Between election and inauguration, the S&P 500 rallied about 6 percent, while most of the country ETFs fell to varying extents.

Within weeks after inauguration, as the breadth and extent of Trump’s tariffs were revealed, most markets fell. Of course, US tariffs were not the only shock moving markets. Notably, Chinese equities rose in response to government stimulus. Trump’s sweeping “Liberation Day” tariffs on April 2, however, provoked a slump in all markets, reversed to varying degrees by the April 9, 2025, 90-day pause.

Figure 2. S&P 500 and Foreign Market Indexes.

Source: Bloomberg and authors’ calculations.

Notes: Each index is normalized to 100 based on its own value on November 4, 2024. This allows for a direct comparison of relative performance over time.

Table 3 shows the percentage change on each valuation day for the S&P 500 ETF (SPY) and ETFs for six heavily affected countries: Mexico (EWW), Canada (EWC), China (FXI), South Korea (EWY), Japan (EWJ) and the European Union (JGK). The first three are the top US trading partners. All six have large bilateral surpluses in their merchandise trade with the US, resulting in high (but falsely named) “reciprocal” tariffs. All ETFs are traded in New York, ensuring that valuation changes occur during the same time period.

At the foot of Table 3 the first row shows cumulative negative losses between November 5, 2024, and April 30, 2025, expressed in percentage terms; the second row shows cumulative positive gains in percentage terms; and the third row shows cumulative positive gains, apart from the surge on April 9, 2025, again in percentage terms.

In percentage terms, the S&P 500 experienced the biggest cumulative losses from Trump’s negative tariff announcements, though Canada and South Korea were close. China and Europe were least affected. Trump’s tariffs dealt a heavier blow to US equity values than to the supposed targets, especially China.

Moreover, foreign equity markets generally enjoyed equal or larger cumulative gains than the S&P 500 from Trump’s positive tariff announcements. Foreign one-day gains, apart from the April 9 surge, exceeded the S&P 500 gains. Worth noting is that cumulative S&P 500 losses, apart from the April 9 relief rally, were almost twice as large as gains. If President Trump wants US equity market to prosper, he should pause more tariffs.

Table 3. One-day price returns of selected ETFs on Trump announcement days. Daily percent changes.

Evaluation Day

S&P500

EWC (Canada)

EWW (Mexico)

FXI (China)

EWJ (Japan)

EWY (South Korea)

VGK (Europe)

11/5/2024

1.2

1.1

-0.1

2.4

1.5

0.4

0.7

1/21/2025

0.9

1.7

1.9

1.1

1.7

1.6

2.3

2/3/2025

-0.8

-1.6

2.5

-0.5

-1.0

-1.1

-1.5

2/10/2025

0.7

0.9

0.2

2.7

0.4

1.8

0.7

3/4/2025

-1.2

-1.7

0.3

1.5

-0.8

0.5

0.2

3/25/2025

0.2

0.5

1.1

-1.0

0.7

-0.4

0.6

3/26/2025

-1.1

-0.8

-1.1

-0.1

-1.3

-0.5

-1.4

4/3/2025

-4.8

-2.3

4.0

-0.9

-4.1

-2.7

-1.4

4/8/2025

-1.6

-1.6

-0.9

-1.4

0.5

-3.7

-0.4

4/9/2025

9.5

6.4

7.9

7.1

7.6

8.9

7.4

4/11/2025

1.8

2.9

0.8

4.4

2.5

4.8

2.7

4/29/2025

0.6

0.2

-2.9

-0.6

0.4

0.8

0.2

Cumulative one-day losses (%)

(9.5)

(8.0)

(5.1)

(4.5)

(7.2)

(8.4)

(4.7)

Cumulative one-day gains (%)

14.8

13.7

18.6

19.2

15.4

18.7

14.8

Cumulative one-day gains (%), without April 9

5.3

7.3

10.7

12.2

7.8

9.8

7.4

Source: Bloomberg and authors’ calculations.

Notes: One-day price returns are calculated by the percentage change between the last price of the evaluation day and the previous trading day. If an announcement is made on a non-trading day, the evaluation will be based on the nearest trading day.